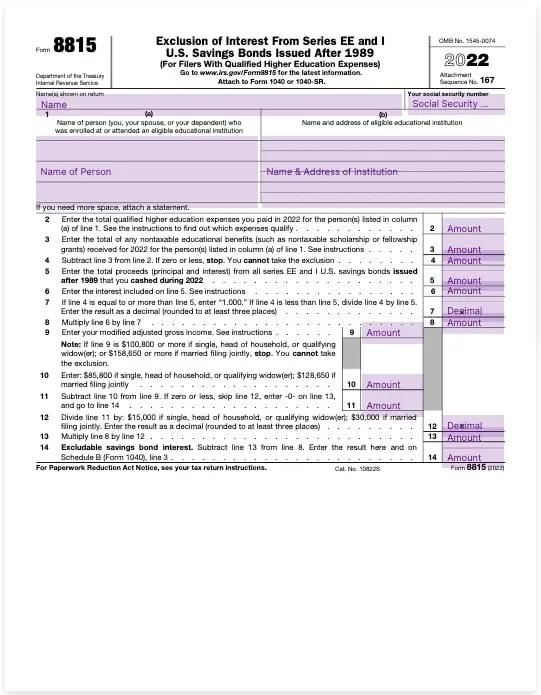

To be eligible for the interest exclusion on Form 8815, taxpayers must meet the following criteria:

- The bonds must be Series EE or I U.S. savings bonds issued after 1989.

- The bond owner must be at least 24 years old before the bond’s issue date.

- The bond proceeds must be used to pay for qualified higher education expenses at eligible educational institutions.

- The taxpayer’s filing status cannot be married filing separately.