Use This Simple Payment Agreement Template

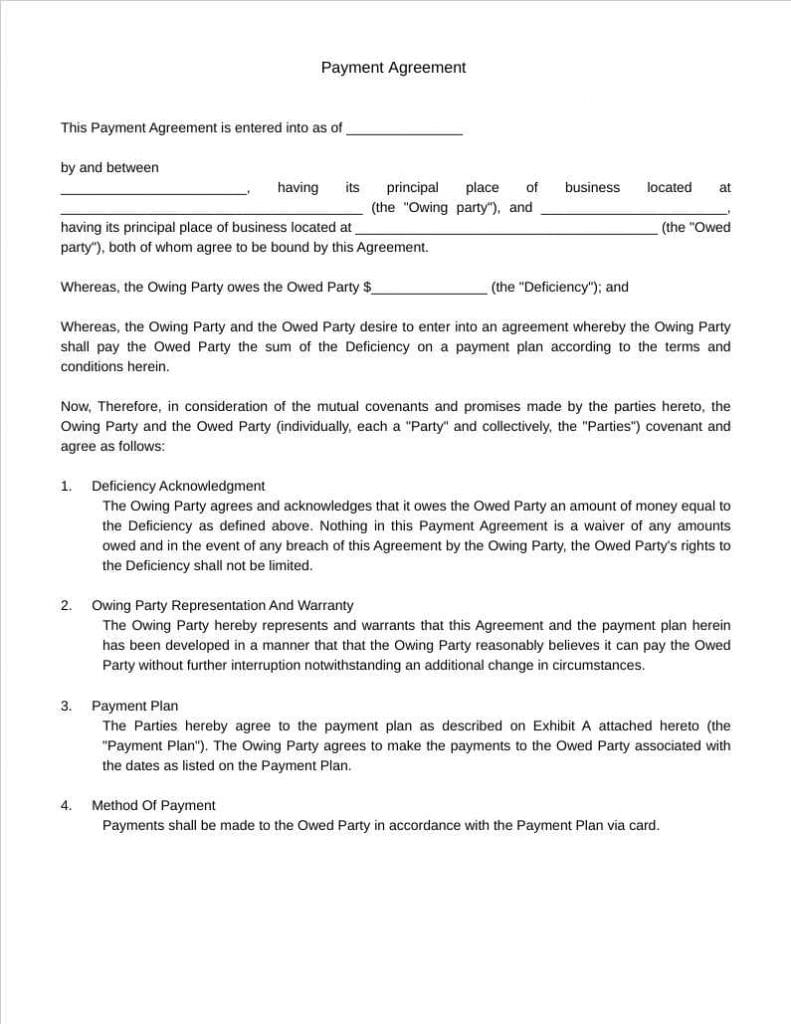

Payment agreements are very important documents that list the terms and conditions of an outstanding balance. Information about the repayment terms, the actual amount owed, and the interest rates are required to be included in this agreement.

A simple payment agreement is a contract between two parties that lays out the terms and conditions of the financial transaction. These agreements are important because they help to establish clear expectations and guidelines for both borrowers and lenders.

For borrowers, a payment agreement can be an essential tool for managing debt and meeting financial obligations. With this legal document, they are obligated to track their loan or payment schedules, meaning they can plan accordingly and avoid overdue payments or fees.

Meanwhile, for lenders, a payment agreement serves as proof of the borrower's commitment to repay their debt. It also allows them to suspend collection efforts if the borrower falls behind on payments, thereby protecting the lender from any potential loss of funds.

In short, payment agreements serve an essential role in ensuring that everyone involved in a financial transaction knows what to expect, helping to foster trust and cooperation between parties.

Easily fill your payment agreements

Paying back what you owe can be tricky, especially if your finances are tight. Monthly payments can help make it easier by breaking down unpaid debts into smaller, more manageable payments.

Our team has worked with lawyers and specialists to develop an easy and effective payment agreement template that can be used by businesses and individuals.

When to Use a Payment Agreement Template

It is important to get a payment agreement in writing, whether you are the lender or borrower. Use a payment plan template whenever you are:

- Planning on lending money

- Planning on borrowing money

- Planning for an amortization or installment plan

- Record the number of payments and interest on a loan

Although a lot of information is required during a repayment process, it can be less confusing if you keep track of the vital data and details in the form of a payment contract. By following a few easy steps and staying organized, you can ensure that your entire agreement is solidified with a legally binding document and that you're following the governing law (depending on which state you're in) when making payments.

Write a payment agreement

When filling out a payment plan agreement, it's important to be as specific as possible to avoid any misunderstandings or confusion.

A fit-for-purpose agreement

Include the parties involved, including names and contact information. Then specify the amount of money being borrowed or lent, followed by an outline of the repayment terms including the payment method.

Simple payment agreement

The payment agreement form should be as simple as possible, clearly stating the terms and expectations of both parties.

Satisfying both parties

Both the borrower and the lender should agree with the terms of the payment agreement, as this can serve as legal proof in the case of a dispute. Include information on interest rates and late payment fees if applicable. Include information on the date of the agreement and when it will end.

FAQs About Our Free Payment Agreement Template

What is a payment agreement contract and how do they work?

In the case of money or payments, the payments are usually made through payment schedule contracts. This is an official written document between two parties, generally known as lenders. It is required to follow certain steps to work efficiently.

Use our template as your basis for an agreed-upon agreement. It is particularly useful when the amount borrowed is large. When a loan is made between a friend and family member or colleague, ensure both parties agree on the conditions and sign their consent.

Why are payment agreements important?

Borrowing funds is a common financial transaction in society. Almost every relationship we have with debt has a source of financial burden. When planning payment arrangements, there are often handshakes and verbal agreements.

Regardless of our intentions, things happen, and sometimes debtors cannot pay the money back. When the payment agreement template cannot be used for the transactions the creditor may not return the amount.

How can I create a personal payment agreement letter?

If you need to come up with a payment plan for an individual, it is important to create a personal payment agreement letter. This document should state the terms of payment including amount, frequency, and method of payment. It should also include consequences for late or missed payments, such as interest or fees.

Undoubtedly one of the best eSignature application available in the market right now. Would love to recommend Fill.